Institutional Insights: Morgan Stanley - Modest Short USD Positioning Ahead of the Fed

.jpeg)

Morgan Stanley - Modest Short USD Positioning Ahead of the Fed

Key Takeaways:

- Options pricing data reveals a shift in investor positions: reduced short NOK (vs EUR), increased long SEK (vs EUR), reduced long EUR, and added short JPY positions.

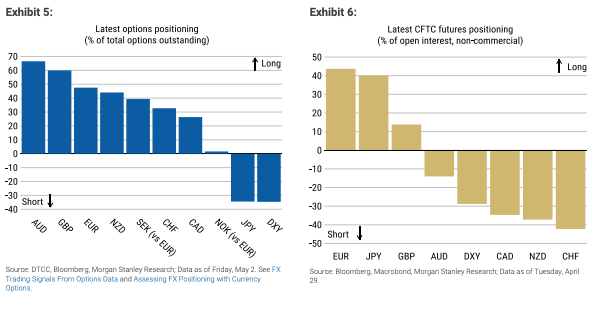

- In the futures market, investors decreased short NZD and CAD positions but increased short USD (DXY) positions.

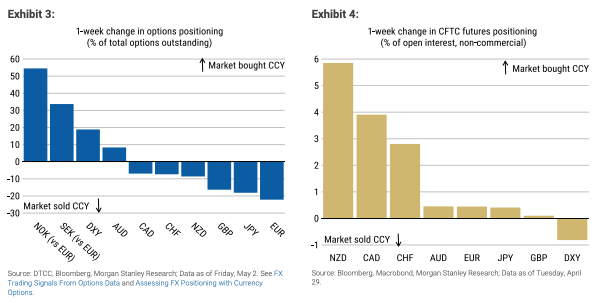

- Overall, options data indicate tactical investors are currently long AUD and GBP, while holding short positions in USD (DXY) and JPY.

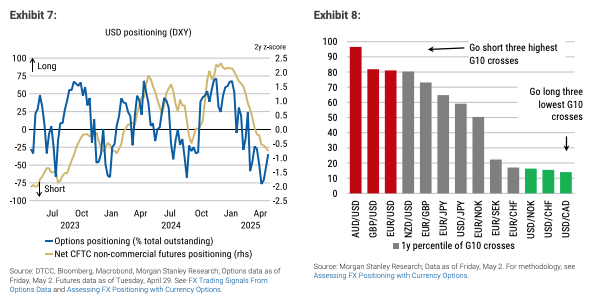

- Futures market positioning shows long EUR and JPY, alongside short CHF and NZD positions.

During the week ending Friday, May 2, options pricing data revealed that investors scaled back short NOK (against EUR) positions while increasing long SEK (against EUR) positions. At the same time, they reduced long EUR positions and expanded short JPY positions (Exhibit 3). In the futures market, for the week ending Tuesday, April 29, investors trimmed short NZD and CAD positions but increased short USD (DXY) positions (Exhibit 4).

Options data indicates that tactical investors are currently holding long positions in AUD and GBP, while maintaining short positions in USD (DXY) and JPY as of May 2 (Exhibit 5). In the futures market, positioning shows long positions in EUR and JPY, and short positions in CHF and NZD as of April 29 (Exhibit 6).

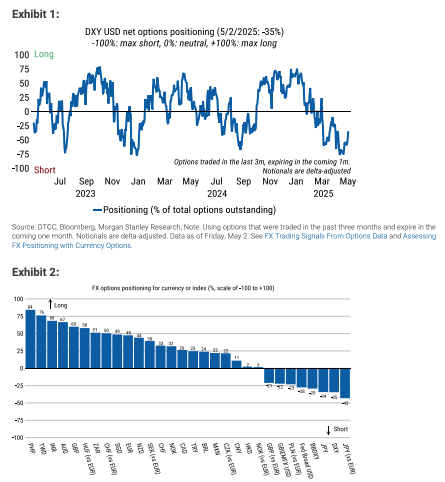

Options and futures market data indicate a short positioning on the USD (Exhibit 7). According to our short-term (weekly) contrarian strategy model, AUD/USD is the favored short position, while USD/CAD is the preferred long position (Exhibit 8).

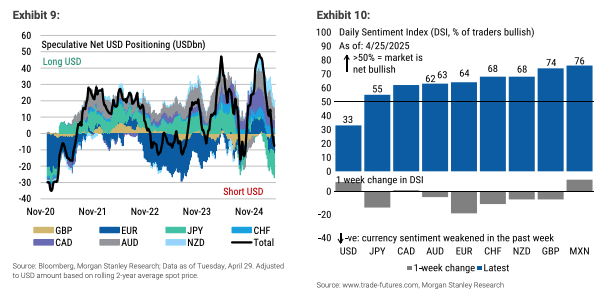

Speculative USD (DXY) futures positioning decreased to -7.6% of open interest for the week ending Tuesday, April 29, down from -4.0% the previous week (see Exhibit 9). By Friday, May 2, the USD and NZD experienced the most significant gains in the Daily Sentiment Index, while sentiment toward GBP and EUR saw the sharpest declines among the G10 currencies (see Exhibit 10).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!