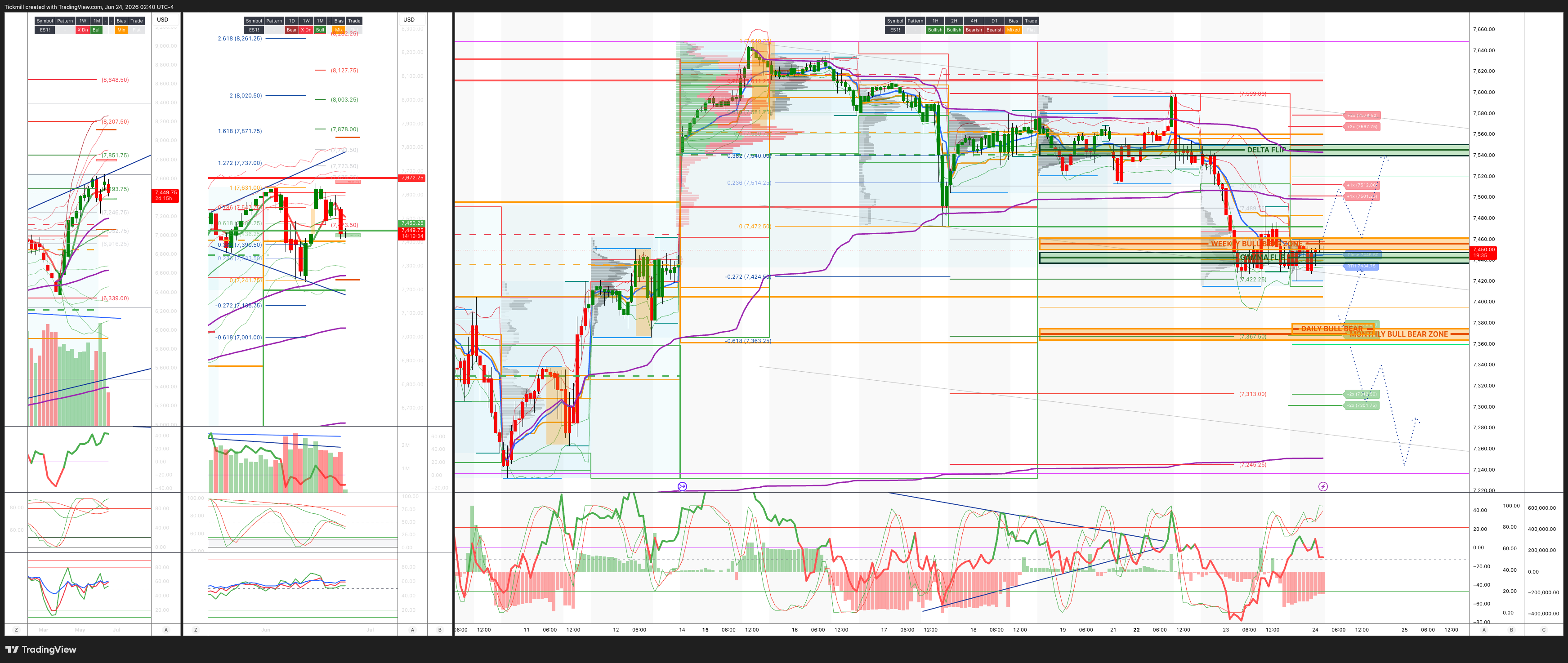

S&P500 Daily Action Areas & Price Targets 24/6/26

S&P500 Daily Action Areas & Price Targets 24/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7560/50

WEEKLY RANGE RES 7692 SUP 7448

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.18 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7573

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFL - 7491

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7377/67

GAMMA FLIP 7443

DELTA FLIP 7511

DAILY RANGE RES 7513 SUP 7377

2 SIGMA RES 7582 SUP 7309

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY/MONTHLY BULL BEAR ZONE TARGET RTH CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Tech Heavy’

Yesterday was a clear AI/Semi-led risk-off session, but still more of a positioning/liquidity unwind than a broad macro panic. The S&P fell 144bps to 7,365, NDX dropped 329bps to 29,347, Russell lost 94bps to 2,976, and the Dow was nearly flat, down 9bps to 51,666. Volumes were heavy at 24.738bn shares versus a YTD average of 19.546bn, and the MOC was a large $5.5bn to buy, suggesting significant end-of-day demand despite the selloff.

The key story was the violent unwind in Asia AI/Semis bleeding into the US session. KOSPI was down around 10% overnight, foreign investors sold more than $2.5bn of Korean equities, and Korean bellwethers traded on record volume. SK Hynix trading $26bn notional, its highest-volume day ever, is a major signal that this was not a normal de-risking day. The levered product ecosystem amplified the move, with 2x levered Hynix trading $3.5bn and closing down 24%. This ties directly to the prior concern that leveraged ETF dealer gamma in Korea can become a major market-flow amplifier on large-move days.

In the US, the pressure landed squarely in Semis and memory. SOX fell nearly 8%, and this was already the 8th daily move of plus/minus 5% in the SOX this month alone. That is an extraordinary level of realized volatility for such an important leadership group. NDX’s roughly 3.3% decline was the third-largest daily pullback of the past year, but the Dow being almost unchanged shows the selloff was heavily concentrated in Tech/AI rather than broad equity liquidation.

The proximate drivers were a mix of positioning, liquidity, and fundamental anxiety. Concerns around recent issuance and potential additional supply hit Asian AI names. Source-of-funds dynamics remain active as investors fund positions across the AI ecosystem by trimming supercap tech and crowded winners. Google-specific concerns around senior AI talent departures remain in the background. MU earnings Wednesday night also matter, especially with the stock lower on T+1 in five of the last six reports, reinforcing the perception that MU is not treated as a clean “earnings stock” the same way some other AI leaders are.

The month-end pension rebalancing estimate is also important. US pensions are modeled to sell around $40bn of US equities, reportedly the largest sell estimate of all time. In a market already dealing with corporate blackout, shallow top-of-book liquidity, and elevated Tech leverage, this creates an additional flow overhang. The calendar is also turning quieter into July 4th, with only PCE Thursday and Russell rebalancing Friday as major near-term catalysts. That means positioning and flow dynamics may matter more than fresh fundamental news over the next several sessions.

The desk tone was notable: activity rose to 5 out of 10, and flows finished -731bps for sale versus a 30-day average of +78bps, with both Asset Managers and Hedge Funds notably for sale, concentrated in Tech and macro products. But the selloff was described as orderly, with no real sense of panic. ETF share of tape began elevated at 36%, but did not reach March peak-volatility levels and normalized through the session. This matters because it suggests forced liquidation was present, but not yet cascading.

Still, top-of-book liquidity remains shallow, which is exacerbating price action. That is one of the biggest tactical concerns. When liquidity is thin, large flows from ETFs, pensions, CTAs, dealer hedging, and levered products can create outsized index moves without a proportional deterioration in fundamentals. Yesterday looked like exactly that: a crowded leadership group hit by positioning pressure in a shallow-liquidity environment.

Macro was not the main driver. WTI fell 69bps to $73.35, which remains a disinflationary tailwind. The 10-year was essentially unchanged at 4.495%, so this was not a rates shock. DXY rose 36bps to 101.38, consistent with risk-off dollar demand and post-Warsh policy support. Gold fell 188bps to 4,111, and Bitcoin dropped 307bps to 62,398, which suggests this was less about classic flight-to-safety and more about deleveraging/risk reduction across speculative and crowded assets.

VIX jumped 13.14% to 19.54, but again, the move was less alarming than the NDX/SOX spot action might imply. The volatility market confirmed the concentration of stress in Tech. NDX vol outperformed sharply, with the straddle realizing around 3x to the downside, while SPX front-end vol was bid but longer-dated vol was little changed. The NDX 1-month implied-vol spread to SPX is now above 10 vols, in the 99th percentile on a one-year lookback. That is a very clear message: the market is repricing Tech-specific risk much more aggressively than broad index risk.

The derivatives flow also fits the “orderly but hedging up” narrative. There were SPX skew buyers and NDX downside buyers, while the desk continues to prefer QQQ put spreads through month-end as the hedge. A large short-dated SMH collar hit the tape, which is exactly the kind of structure expected when investors still want to retain Semi exposure but need protection after a violent move. Meanwhile, some customers defended select megacap names with upside-vol expressions, suggesting investors are not abandoning the theme entirely.

The key tactical question is whether this is a reset within the AI bull trend or the start of a deeper deleveraging. For now, it looks more like a positioning shock than a fundamental break. Oil is lower, rates are stable, credit has not been highlighted as stressed, and the selloff is concentrated in the most crowded, levered, high-beta parts of AI. But the magnitude of the SOX and Korea moves is large enough that investors should not dismiss it. When leadership groups start realizing this much volatility, gross exposure often has to come down even if the long-term story remains intact.

The next major catalyst is MU earnings. The market is now more fragile going into the print. A strong report with clean HBM demand, pricing, supply discipline, and constructive guidance could help stabilize memory and Semi Equipment. But given the recent positioning and the stock’s weak post-print history, a merely “good” report may not be enough if investors are focused on valuation, capex sustainability, and crowded exposure. MU is less likely to be judged on the quarter alone and more likely to be judged on whether it can restore confidence in the broader memory/AI infrastructure trade.

PCE on Thursday also matters because Warsh’s Fed has made inflation data relevant again. If PCE is benign, lower oil plus stable rates could help risk stabilize. If PCE is hot, the market loses one of its key offsets to the AI positioning unwind, and front-end pricing could re-tighten. Russell rebalancing Friday adds another layer of technical flow risk, especially for small caps and ETFs.

Implied ranges

SPX implied move: 0.83% So the SPX implied range is approximately 7,304 – 7,426

QQQ / NDX proxy implied move: 1.6% So the NDX-implied range using the QQQ move is approximately 28,877 – 29,817

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!